Junior Bankers’ Raises Widen Record Pay Gap Among College Grads

August 13, 2021

August 13, 2021

LINK TO ARTICLE HERE

Much of Michael Lewis’s graphic description of life for junior bankers in the early 1980s still rings true today. Fresh college grads “gave themselves over entirely” to firms, working so many nights and weekends that one friend learned to nap on the office toilet, the author recalled in his semi-autobiographical “Liar’s Poker.”

But one thing is changing fast: The pay.

A recent wave of raises meant to address complaints that rookie bankers, known as analysts, work too hard for too little means this year’s newbies will get salaries of at least $100,000, before five-figure bonuses.

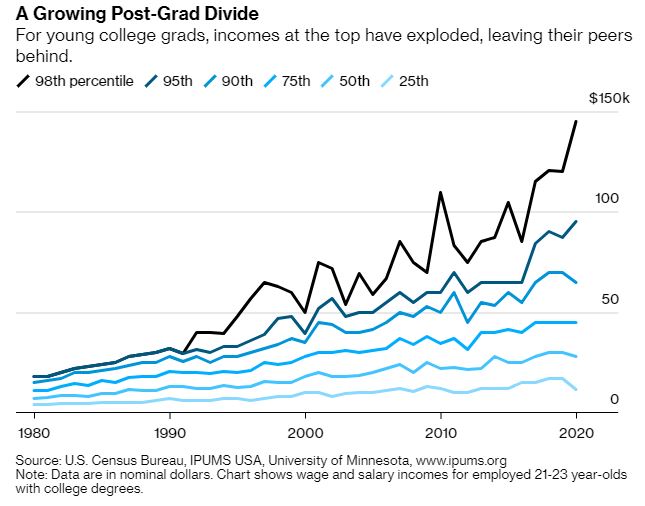

Amid an escalating U.S. debate over income inequality, junior bankers are now on track to earn almost five times — or more — the median wage of fellow young college graduates, Census Bureau data show. Back when Lewis comically bombed his initial interviews to join Wall Street, he was chasing the prospect of earning what he saw as a whopping $25,000 salary, about twice the median then. Adjusted for inflation, it translates to roughly $72,000 now.

Such comparisons deliver a reality check for two raging debates: One on Wall Street over work-life balance and another across the U.S. focusing on the widening gap between wealthy and poor workers, an increasingly hot topic in Washington.

After junior bankers were pressed to do even more during the pandemic, virtually every firm — including Goldman Sachs Group Inc., JPMorgan Chase & Co. and Bank of America Corp. — sweetened their paychecks. On top of that, some industry leaders offered fresh assurances that newcomers would have manageable workloads, regular sleep and at least some Saturdays off. That’s prompted grumbling from some veterans who see the notorious rigors of the analyst track as a rite of passage.

The advances, fair or not, mean junior bankers are pulling further ahead of their counterparts in a long list of other professional fields, where wages have stagnated for decades under pressure from automation, globalization, weakened labor power, a deepening pool of college graduates and other economic forces.

Banking is now among just a few industries — including technology, engineering and consulting — that together account for the vast majority of jobs in the top 10% of entry-level salaries, according to data from Glassdoor. And successful junior bankers enjoy ample prospects to keep growing their income for years to come.

So while they might start setting aside savings for a mortgage, many contemporaries will struggle to pay off student loans.

Attending college was long one of the most reliable ways to earn a good living. By 2000, the premium for getting a college degree after high school jumped to 65%, up from 40% in 1980, according to an analysis from economists Claudia Goldin, Lawrence Katz and David Autor. But since then, it’s hardly budged.

In fact, their research shows, virtually all of the increase in income inequality this century comes not from the gap between college and high school grads, but among college grads themselves. Since 1992, wages hardly changed or even declined for graduates who earned less than the median in the workforce, when adjusted for inflation.

Meanwhile, pay in the upper bands rose dramatically. Year after year, investment banks were among those shelling out more as they vied with ascendant Silicon Valley giants for the best candidates and tried to head off poaching by investment firms, such as buyout and hedge funds. College grads are particularly valuable to tech firms, because they’re trained on the fast-moving frontier of computer science.

Banks didn’t face that competition when Lewis first applied, as modern training programs were still taking shape at many firms. Indeed, the $25,000 figure he cites in his chronicle of that era might be too generous. Several bankers who received or accepted offers from major firms around the same time said salaries for junior bankers were thousands less — which makes the jump to $100,000 all the more dramatic.

Banks are willing to pay more to recruit the most elite candidates, in part because executives are convinced that “exceptionally able people are always in scarce supply,” said Anthony Keizner, a managing partner at recruiting firm Odyssey Search Partners. It doesn’t matter if colleges’ graduating classes have swelled because banks are setting their sights on the valedictorians, he said.

“People in finance aren’t being hired just because they’ve done econ and accounting and come in with Excel skills,” he said. Banks “are interested in the best of the best.”

The current debate over analyst pay erupted after recruits were forced to sequester to tiny apartments or with parents back home during the pandemic, straining to keep up with demands for slide decks as economic turmoil drove a deluge of corporate deals. When trainees at Goldman drafted a presentation detailing the brutal demands on their time, it leaked to the internet and all hell broke loose.

Soon, Morgan Stanley, Citigroup Inc., Deutsche Bank AG, Barclays Plc, Evercore Inc., Guggenheim Partners, PJ Solomon and Nomura Holdings Inc. were also among firms that announced raises.

Some bankers from modest backgrounds say they appreciate that Wall Street is a place where hard work can pay off.

David DeFronzo recalled parking his grocery delivery truck mid-route in 2009, leaving the keys in the ignition to keep the refrigerator running while he attended his high school graduation rehearsal. His grandfather had recently died, his father was out of work and his parents had lost their home just north of Boston.

He eventually saved enough for community college, and while there landed an internship at State Street Corp. He’s grateful for the shot it gave him.

“It’s all perspective,” said DeFronzo, now 30. “Relative to waking up at 3 a.m. to drive a truck through 12 p.m., going to school and washing dishes overnight, the workload was a lot easier.”

He eventually earned a degree from the University of Massachusetts and moved on from State Street in 2017, jumping to Grant Thornton.

DeFronzo’s ascent is atypical. Many junior bankers hail from families that are well off or have deep ties to the industry, giving them an advantage in interviews.

“For a wealthier classmate who grew up summering with their parents’ colleagues, it’s sort of a natural social exercise,” said Tara Falcone, a former hedge fund analyst who founded ReisUP, which advises low-income college students on personal finances.

She said she grew up poor and was the first in her family to go to college, graduating from Yale University. “People from my background are told growing up not to ask for handouts, not to use people,” she said

That social divide can dissuade some from applying to Wall Street, despite the $100,000 salaries.

“It makes more sense to say, ‘If I learn to code really well, I can get a job,’ rather than trying to navigate a social space,” said Victoria Garcia, 20, a rising junior at the University of Pennsylvania and finance and operations chair of Penn First, a group for first-generation, low-income students.

When the organization held a career information session with representatives from tech, consulting and investment banking firms, finance drew the smallest crowd, she said. “There’s a general sense of, ‘That is not what I want to do, that is not where I belong.’”

Article by: Eric Krebs

Future Formation – Exploring The Options

Future Formation – Exploring The Options